The “Location, Location, Location” mantra intended to mean the three things that matter most in real estate should be replaced by “Valuation, Valuation, Valuation.”

Valuation is the foundation of a successful CMBS deal and key to setting expectations, from cash flow to recovery. It should take paramount importance in times of economic flux because when, as now, there is uncertainty and the potential for losses, it is the area where deal parties may be most vulnerable to legal claims by investors, including ones related to special servicing practices, net operating income (NOI) and property appraisals.

In fact, valuation issues have already become the center of litigation and are impacting the ability to refinance in a rising interest rate environment.

Refinancing Challenges

There is a looming wave of $97 billion in CMBS conduit loans maturing in the next 36 months, with $33 billion coming due within the next 18 months. It’s a smaller wave than the great “Wall of Maturities” from five years ago, but as I discussed with Wealth Management Real Estate recently, it could have a disproportionate impact given rising interest rates and the likely increased costs and, at its core, it can create valuation uncertainty.

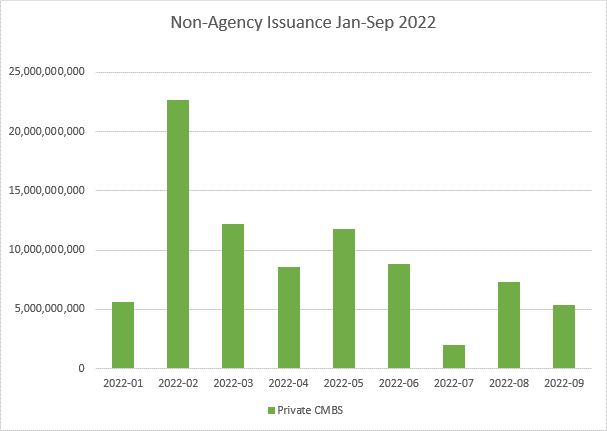

CMBS’s response to rising interest rates can be a bellwether for the economy given cash flows are indicative of the health of so many sectors of the economy, from retail to industrial. So far, interest rate volatility has introduced further uncertainty to the shifting sands of a post-pandemic economy, and by extension, the secondary market. As I indicated in a recent interview in Commercial Property Executive, the uncertainty for both lenders and borrowers is reflected in widening credit spreads and the sharp drop in new issuances in June and July (since the war in Ukraine started), after a good start to the year.

(Bloomberg data, provided by Stout)

For the most part, there has been steady improvement in delinquencies since pre-pandemic peaks, but when it comes to interest rates, there is a tipping point when too high becomes too much and negatively affects property values and underlying credit performance. For maturing conduit loans averaging 4-5% capitalization rate, analyses have shown a good portion of them being able to maintain an acceptable debt service coverage ratio (DSCR) and obtain refinancing at 6-7%. At higher levels, there is a greater chance that more expensive additional layers of debt will be needed.

Eyes on Office and Retail

Across sectors, there will be refinancing challenges for properties with already low NOI relative to existing debt. Not only are they maturing into a higher rate environment, but other costs are going up as well, including the cost of interest rate cap insurance and maintenance.

According to DBRS, by sector, retail and office comprise the largest portion of loans maturing in 2022-2023. These sectors have been tested and strained by Covid. If there is a recession, as some have predicted by end of 2023, then aside from higher interest rates, valuations can shift, dropping NOI below desired or viable levels for refinancing.

Particularly in the office sector, remote and hybrid work and the success of employers’ return to office plans will impact whether refinancing or extension is available for a given property and impact valuation. Potential changes in office use would exacerbate excess supply issues generally, but disproportionately impact older buildings, which could find it even more challenging to refinance. Manny Malbari, Structured Finance Practice Co-Leader, Valuation Advisory at Stout, notes a good example of this is “NYC where tenants are signing new leases with a smaller footprint in new buildings with better amenities than their existing space to attract and retain talent.”

Challenges are compounded by the fact that lease agreements on some 900 million square feet of office space in the US are set to expire by 2025, which could result in a significant loss in value over a number of years.

Retail is subject to further distress given inflation, supply shortages and changing consumer preferences and will not stabilize all that quickly.

Special servicing of distressed loans can make or break distressed CMBS deals. Gunes Kulaligil, Structured Finance Practice Co-Leader, Valuation Advisory at Stout points out that “the goal should be to maximize the value to the trust as a whole. Both the dollar amount and the timing of recoveries matter if the disposition route is chosen. However, various types of modifications may provide more value than property disposition.”

Whichever resolution is chosen, it will be important to show this was the “best” outcome for the trust. “The issue, of course is, different parts of the capital structure will end up better-off or worse-off depending on how much of it is received, when and what it is called based on the underlying agreements,” warns Kulaligil. To complicate matters, sometimes servicer and junior bond holders may be affiliated or even the same entity “further highlighting the importance of providing a clear rationale and the NPV analysis for any resolution strategy,” Kulaligil suggests.

Valuation Litigation

To Kulaligil’s point, Icahn Partners v. Rialto Capital Advisors, LLC is a 2022 Nevada state court dispute between certificateholders and a special servicer over an outlet mall property demonstrating the critical role of valuation and its impact on legal exposure.

The complaint describes the underlying agreement as having a control-shifting mechanism whereby the first-loss Class E certificateholders with more than 25% certificate balance outstanding assume control once implied losses are ascertained. This is rooted in the principle that the most exposed certificateholders should have control of what happens to the property backing the certificates.

Plaintiffs are the Class E certificateholders that claim the special servicer denied them control of the property by ordering artificially inflated appraisals that did not properly reflect certificateholder implied losses. They allege the special servicer’s maneuver was prompted by its desire to salvage the property and to keep operating it although a sale would have been the rational course of action to mitigate the certificateholders’ losses.

While the case is in its early stage, with a pending motion to dismiss, it’s a scenario that shows the changing fortunes of one deal based on a valuation as interpreted under the contract.

Conclusion

Valuation will be a paramount consideration given the turbulence in the market, especially in the office sector. If performance does weaken and there are battles over loss allocation, valuation disputes are likely to be at the center. Market uncertainty and losses may seed fertile ground for disputes over projected NOI and occupancy levels, and the role of valuation in setting key loan ratios such as DSCR and loan-to-value.